Money can't by me love :)

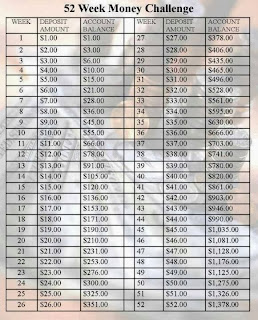

I was perusing Pinterest one day and I stumbled upon this picture, claiming to save SO much money over one year!

See, they wow you by the simplicity of starting out, saying that first month you have to put back only ONE DOLLAR and then shows you how much you'd save if you just increase that by one dollar each week for the year! That's almost $1400 dollars wow isn't this easy?!

Well...good question. In the grand scheme of things, is $52 that much? That's the most their asking you to set back!

Well here's my question: If that's not too much to set back, why aren't you setting it back every week? Let's talk if you get paid once every two weeks. That first paycheck you only have to set back $3. That last paycheck you have to set back $103. I'm very curious as to where that extra $100 is going to come from...I don't know about you but I don't make enough to set $100 back with any paycheck.

Call me crazy but if you have $100 that you can set back each paycheck, you should be setting that back, not only $3 because some challenge told you that's all you need to set back. Think about it this way: Would you rather have $1400 in savings or $5200 in savings?

I win ^_^

Here are MY tips (translate: the tips my mother is begging to drill into my head) for saving money:

1) If your goal is just to build a savings, set back 10% of each paycheck. Put it in an account that you can't/won't touch. I make approximately $1600 a month currently. If I set 10% back for a year, I would have $1560 in savings. Not only is that more than this 52 week challenge, but it's a fixed rate. Fixed things are easier to get used to, we like those.

2) Know what needs to get paid each month and WHEN. If you have a rent payment, a car payment, cell phone bills, insurance, know when each thing is due and what paycheck needs to be allocated for it. Knowing what you need to have money for will help curb your desire to spend recklessly. If you need to, write it down. Keep it on your fridge, on your car visor, in your phone, wherever you need to in order to make your spending a conscious action.

3) A late/missing a payment is not worth bad credit. period. end of story.

4) It is a lot easier to consciously spend by paying in cash rather than with a debit/credit card. First, paying in cash means you have to get cash, meaning to have to make the conscious effort to go to your bank or ATM. Then when spending, you physically see how much money you started with and how much you have after your spending. It might make you think twice about if you really need that candy bar at the check out or not.

5) Have a coin collect jar. The good thing about paying in cash is that you get change back. Have a bowl or jar where you put all your change to collect, and then come up with a fixed time (i.e.: twice a year, on your birthday, only when it's full, etc) to cash it in. My mom always said use this money on something nice/fun for yourself. If you think about it, this is your savings (well, hopefully not all of it). While the big savings can be for those big important purchases, this savings can be for you.

6) Don't be discouraged if it takes time for everything to mesh well together. There will be months where you can't put 10% into savings because your car broke down or you needed a new dishwasher. Don't let those bad months stop you from saving all together.

7) Put back what you can, when you can. Even if it's just $15, in the grand scheme of things, every dollar counts.

Hopefully you'll find these to be more practical and a better use of your paycheck.